Nothing like this had been done before.

But despite being fraught with incredible human risk and collateral, the U.S. government went all in.

And institutional capital followed.

It was one of the most bizarre side effects of the pandemic: The disappearance of price discovery for the most promising pre-product-revenue biotech companies.

By mid-2020, institutional capital had become infatuated with any companies associated with Operation Warp Speed.

We may recall this was the public-private partnership funded by the U.S. government to accelerate the development — and ultimately the emergency use authorization (EUA) — of COVID-19 “vaccines.”

The impact of what happened is easy to see on a chart of biotech company Moderna (MRNA)…

Or a chart of BioNTech (BNTX), the company behind the Pfizer COVID-19 “vaccine”…

5-Year Chart of Moderna (MRNA)

5-Year Chart of BioNTech (BNTX)

Both companies rocketed higher from their pre-pandemic levels, on what would certainly be billions in future revenue — revenue generated by the mandates and coercion used by governments and health agencies around the world to take the “vaccines.”

Then the air was sucked out of a room.

The most promising pre-product-revenue biotech companies — with the most compelling technology and therapeutic pipelines — received no love from the markets.

There was little interest in anything other than COVID stories, with awareness fueled by the global censorship industrial complex. Almost everything else declined.

Institutional capital flowed out.

It was as if they were left for dead, despite having capital, intellectual property, and great roadmaps for future drugs to help manage and/or cure human disease.

This resulted in many biotech companies with negative enterprise values.

This is possible because the cash that these biotech companies held was/is greater than their market capitalization. [Note: Enterprise value is simply the market capitalization plus debt, less cash.]

The calculation makes sense.

The enterprise value is the value of the company as seen by the market. That’s because it is so heavily influenced by the market capitalization of the company (share price times number of outstanding shares).

But despite that, those valuations made no sense at all…

How could a promising, well-funded company with an incredible pipeline be trading for less than the cash that it has on its books?

It happened.

And it’s still happening.

The pandemic policies made it extremely difficult for biotech companies to conduct clinical trials. (I discussed this here, in my December 5, 2023 issue of Outer Limits.)

After all, people simply wanted to avoid the hospitals.

Hospitals and clinics certainly had plenty of time and capacity to support the trials, but they couldn’t get people to consistently come in for their course of treatment required by the trials.

That lead to a dearth of data reporting, which meant that there was even less information for institutional capital to determine if progress was being made, or not, at any given biotech company.

It was a stalemate.

Biotech companies knew the value of their programs and their intellectual property. But institutional capital couldn’t figure that out because the biotech industry wasn’t functioning in the way that it normally does.

Which led to lack of price discovery.

Said another way, the valuations of so many biotech companies simply didn’t mean anything at all. They actually weren’t an accurate reflection of what the companies were/are worth. And this situation still largely persists today.

Many thought that with such depressed valuations, the mergers and acquisition (M&A) market would be thriving. They thought that companies would be bought up left and right with such attractive prices.

But the opposite was true.

The boards of the biotech companies and their long-time venture capital backers would never sell out at those irrational valuations.

Lots of attempts were made, but very few offers were accepted.

This is precisely why watching the biotech M&A (mergers and acquisitions) market is so useful.

One of the easiest ways for us to determine that the biotech market is coming back to life is when deals start happening again.

I’m happy to say, that time has come.

In January every year, arguably the most important event in the industry, the J.P. Morgan Healthcare Conference, is held in San Francisco.

It is an invite only event for biotech executives, institutional capital, J.P. Morgan clients, and J.P. Morgan’s own high net worth investors. And it has always been a place where big deals are announced.

During the pandemic, for three years in a row, the conference sadly morphed into a series of Zoom calls. Nothing in person. It was awful, and the deal volume dried up.

No longer, though — the deal flow is back.

In fact, four major deals were announced during the week it was held this year: January 8–11, 2024:

But those four deals don’t tell the whole story.

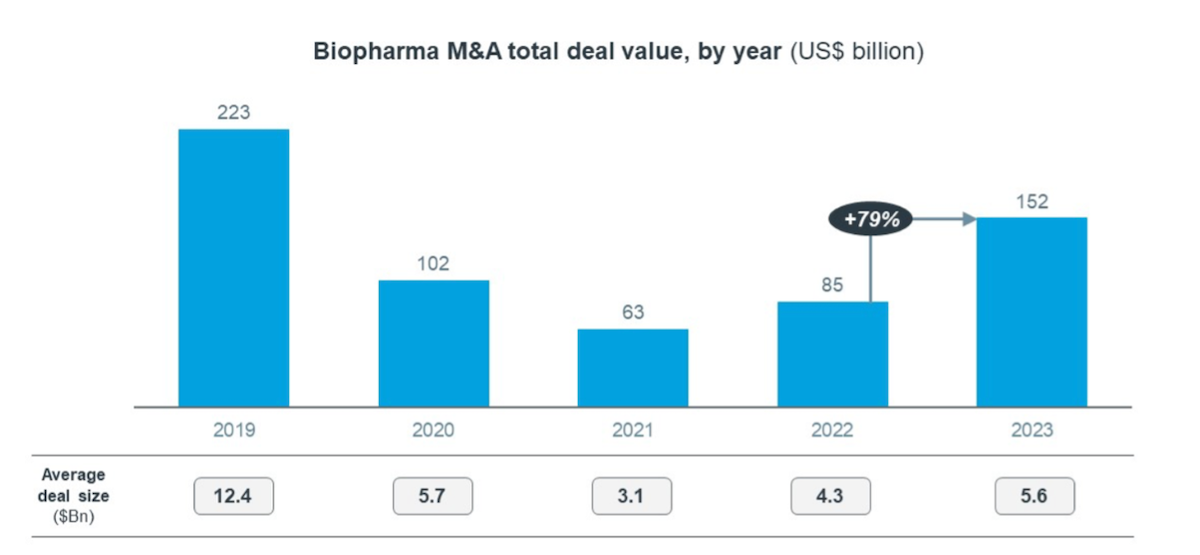

There was actually a deluge of deals that took place between late September through the end of December 2023…

Which kicked off — what I believe is — the beginning of the biotech sector’s rebound back to life.

In total, 15 deals worth a whopping $56.7 billion took place during that short window — a window that I consider to be the most important 4-5 month period of the year for biotech. That’s worth noting!

We can see in the above chart that sharp rebound in 2023 compared to the prior two years.

My expectations for 2024 are for another material increase year over year.

I can’t help but think of an image of a bull standing over the biotech sector with a defibrillator in tow — “clear!!!”

We have a pulse.

And just because almost $60 billion in M&A took place between September and January already… doesn’t mean it’s over.

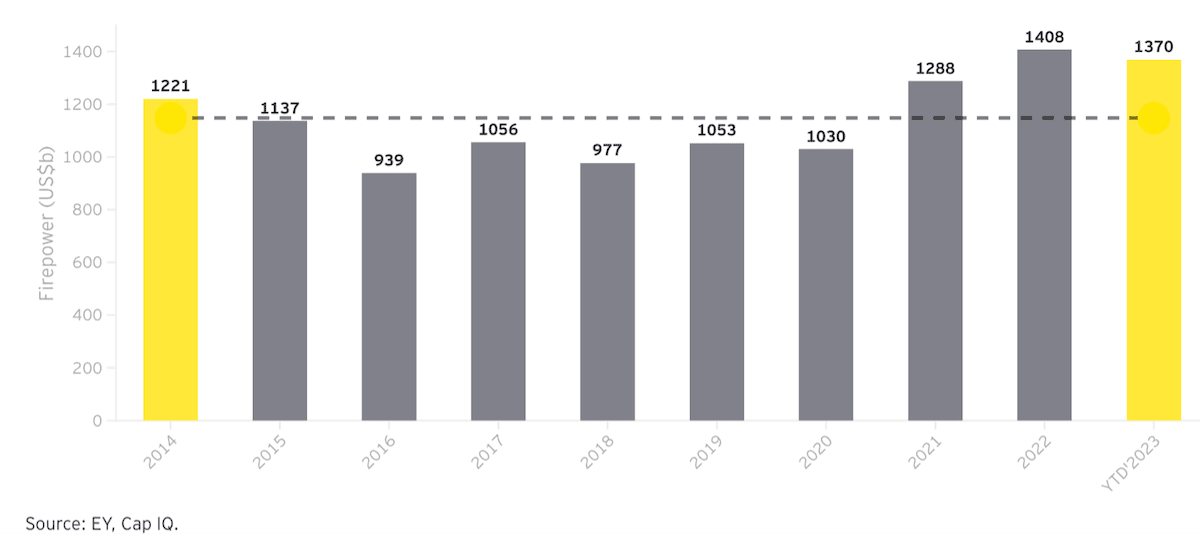

The reality is that the biopharma industry is sitting on an almost unbelievable $1.37 trillion in dry powder — that’s capital capable of being deployed for acquisitions.

In the last 10 years, that’s the second largest “war chest” on record.

Biopharma Industry Dry Powder by Year (in US$ Billions)

And that means that there is a lot more excitement to follow this year.

Clinical trials are now back on track — similar to the levels we had pre-pandemic.

That has resulted in a dramatic improvement in the regularity of data reporting on therapeutic pipelines.

Biotech companies are beginning to get strong market reactions to positive reports, resulting in sharp increases in share prices.

And as interest rates begin to decline, this will be like a shot of adrenaline into the broad biotech sector, and small cap growth stocks in general.

And that means that price discovery will continue to improve, share prices will rise, and we’ll see a whole lot more M&A deals for biotech.

Based on my overall outlook on 2024, which you can read here, interest rates won’t come down nearly as much as most have predicted.

But the good news is, it won’t take much.

Small declines in Fed Funds rates later this year will begin the process of institutional capital flowing back into the biotech sector.

And what comes after that will be epic: A multi-year, raging bull market for biotech… fueled by immense investment and the employment of artificial intelligence in the drug discovery process.

This will be an intense area of focus for Brownridge Research in the years to come.

We’ve already entered the golden age of biotech, most just haven’t realized it yet.

We have so much to look forward to.

What do you think of this issue of Outer Limits? As always, we welcome your feedback and questions, and look forward to them. We read each and every email and address common questions in the Friday AMA issues. Please write to us by clicking here.