Happy New Year!!!

It’s always exciting to the turn the page and begin a new year. Especially after a string of very tough years in 2021, 2022, and 2023.

It feels like discarding some heavy luggage that we’ve suddenly realized we no longer need.

It feels great to let it go, and even better to move forward with a renewed lightness of being.

And it seems I’m not alone in my optimism!

Even the markets entered 2024 with a joyful spring in step.

The S&P 500 closed the year with a 24% gain. The Dow posted a near-record year — up over 13%. And of course, the tech-heavy Nasdaq soared an astounding 43%. Looks fantastic, right?

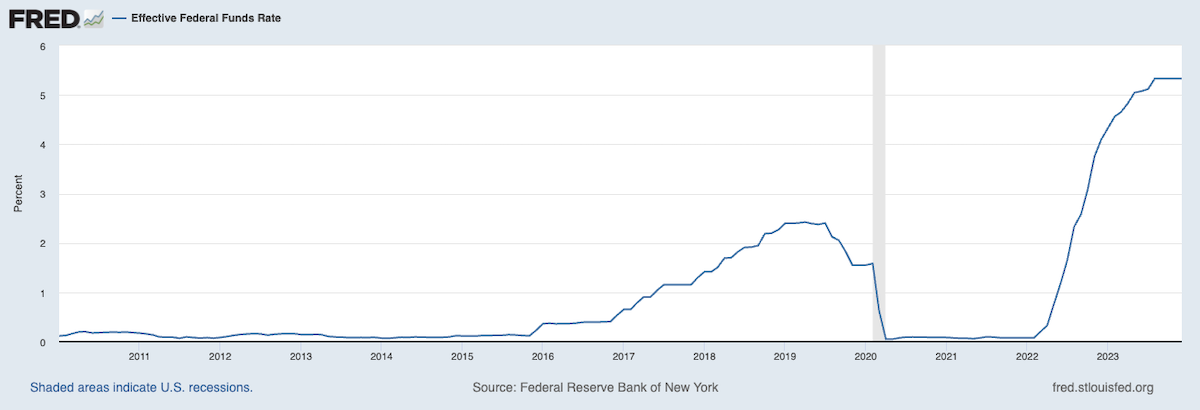

And of course, we aren’t forgetting that the Fed has implied future rate cuts are ahead this year… and we know how the markets like lower rates…

To that end, I thought we’d have some fun looking at the year ahead of us.

What kind of year are we in for? And what does that mean for the economy and for investment opportunities?

If only the optimism was matched by reality.

How I wish I could say differently…

But we’re in for a bumpy ride this year.

Making matters worse is the ever present election year in the U.S., which comes with all sorts of nonsense, distortions, and politically driven policy making.

And while the political circus is always painful to watch, we’d be unwise to look away.

We have to consider how much is a stake.

The reality is that governments around the world have become far more heavy handed in using policy to influence or manipulate the economy and stock markets.

That’s precisely why we need to stay on top of these matters.

Being better informed allows us to make better decisions as investors.

And while there’s certainly a lot of good news as we enter the new year, the truth is that much of it is surface level.

As we enter the year, the good news is that we have seen some improvement in the reduction of inflation. On the surface, at least.

As I’m sure we all painfully remember, the Federal Reserve hit a record pace of Fed Funds rate hikes over the last couple of years.

The goal of the Federal Reserve was simple…

By rapidly increasing the Fed Funds rate, it would reduce consumer demand by causing economic pain. After all, higher interest rates ultimately reduce discretionary spend.

We certainly have felt the pain.

But the truth is: There were other factors at play that contributed to an inflation reduction — factors that are unique to the last few years.

The reality was that the pandemic policies resulted in a massive dislocation of supply chains around the world.

It was a wakeup call for the Western world to realize how vulnerable their supply chains had become.

Everything from electronic components to semiconductors, materials, pharmaceuticals, automotive components, etc. were disrupted.

And when a sudden decline in supply happens in the face of increased demand, prices tend to skyrocket. And that’s precisely what happened.

The good news is that as we enter 2024, these problems have largely been addressed.

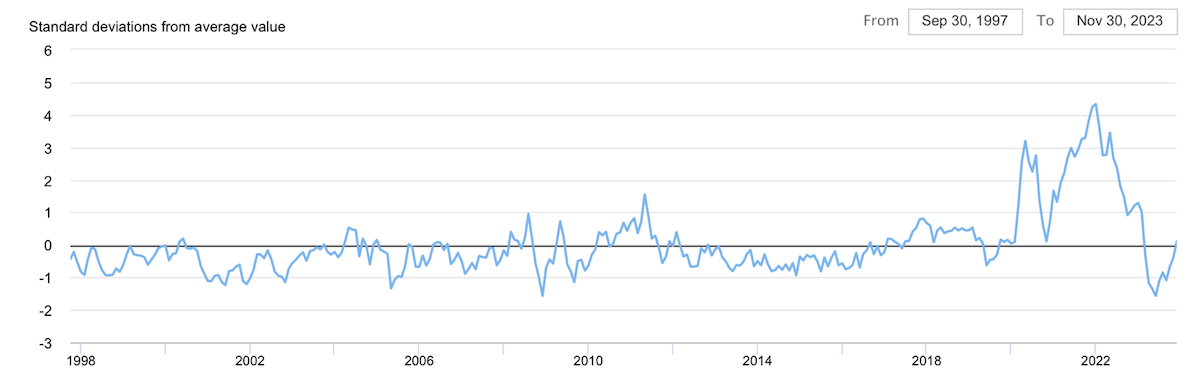

A good proxy to demonstrate this is the following index produced by the Federal Reserve Bank of New York:

Global Supply Chain Pressure Index

Above, we can see an index for global supply chain pressure.

When the index gets out of whack, it spikes upwards. And when there is little to no pressure, it drops below zero.

We can easily see the immediate spike in early 2020 caused by the lockdowns. It dropped for a short period of time, as most of the world was in a panic about what to do… and many of us were suddenly stuck at home.

Then the stimulus kicked in.

Demand went through the roof… and supply chains experienced massive distortions and labor shortages resulting from — and caused by — failed pandemic policies.

Again, fortunately, these issues have resolved. And these distortions returned back to normal last year, as the pandemic policies were lifted and most labor shortages resolved.

Speaking of labor… that was the second dynamic that had an outsized impact on inflation.

There is some important nuance here to understand…

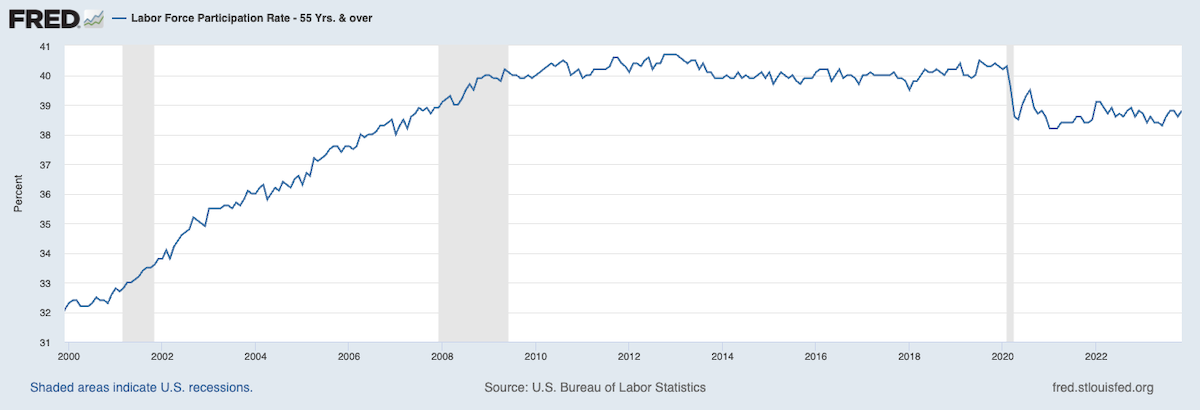

In order to see what has happened, we’ll need to split the labor force into two categories: 25-54 year olds… and 55 years and older.

Above we see the labor force participation rate for those 55 years and older.

We can see the precipitous fall in early 2020, which makes sense.

But what is really striking in the above chart is that participation in this demographic hasn’t recovered since the initial shock of the pandemic. We haven’t seen such low levels of participation like this since 2007.

What this tells us is that — in large — this demographic just quit. And they haven’t come back.

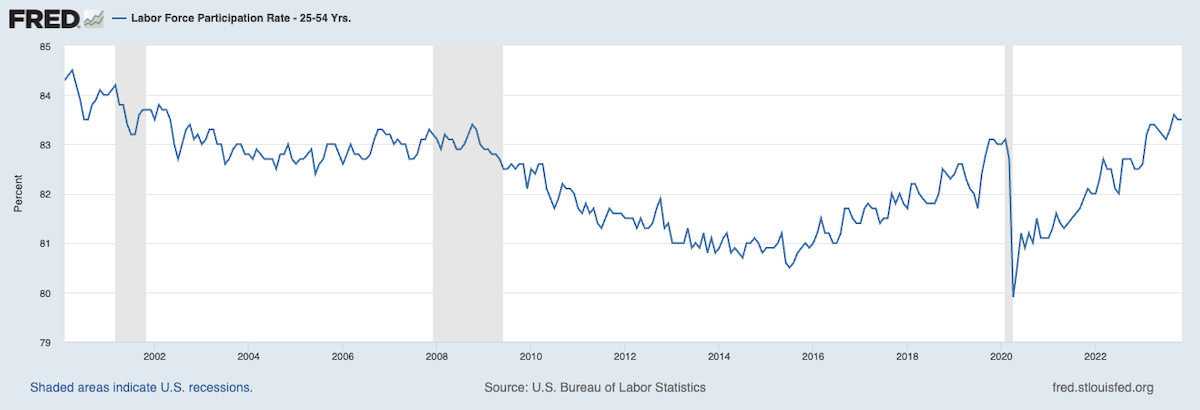

The good news, however, is that the 25-54 age group did return to work.

As we can see in the image above, this demographic not only got back at it, but it also returned to participation rates above where we were in 2019.

For this to happen, we saw wage levels increase significantly, which has contributed to the persistent and non-transitory inflation.

This context is very important for us to understand.

These two massive issues — supply chain problems and labor shortages — were the largest contributors to inflation, outside of massive, debt-fueled government spending (i.e. printing money).

Again, the good news is that these issues have largely been resolved.

However, this also means we shouldn’t expect any further improvement/reduction in inflation from labor and supply chain improvements.

And here’s where all the good news starts to look a little less good.

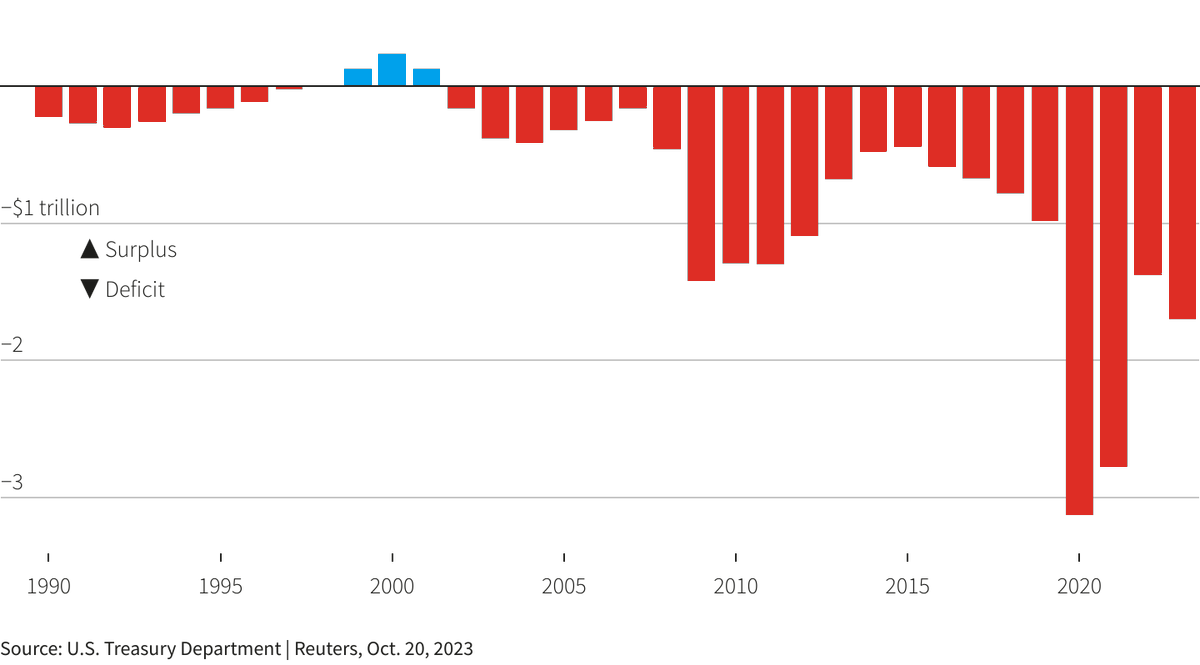

The ugly truth, as we look into 2024, is that grossly irresponsible fiscal deficits have gotten worse, not better.

Above we can see the two massive fiscal deficits that were driven by the absurd overreaction to the pandemic in fiscal years 2020 and 2021. (Note: 2020 US fiscal year ran from Oct. 1, 2019 until Sept 30, 2020.)

That was bad enough. But fiscal year 2022 had a deficit of $1.375 trillion.

And fiscal year 2023, which just ended September 2023, increased by 23% to an even more astounding $1.695 trillion.

For perspective, U.S. government annual revenues from taxes were $4.439 trillion. That means that the federal deficit for FY2023 was equivalent 38% of U.S. government annual revenues.

We should all be shaking our heads.

Despite the U.S being the largest economy in the world, it doesn’t have the money to pay for this kind of spending.

So how did it fund the deficit spending?

The answer is: Debt, and lots of it.

The U.S. government has been “printing” money at a pace never seen before to fund these extraordinary fiscal deficits. And now, as of January 2nd, the U.S. has $34 trillion of debt. Unbelievable.

And while we don’t yet have final GDP numbers for 2023, the debt-to-GDP ratio will almost certainly exceed 125% as a result of this ridiculous spending.

What does this mean? Just the interest payments on the debt have now exceeded $1 trillion as of last October.

Interest payments on national debt have doubled in just the last two years. And at the current pace, interest payments will exceed $10 trillion in less than 10 years. It’s a complete house of cards.

But in the short-term, the real question is whether or not we think that the U.S. government will aggressively reduce its deficit this fiscal year… and embrace fiscal austerity to reduce its debt and deficit. I think we all know the answer to that.

There is no way in hell that’s going to happen.

So, how does this all come into play in 2024? Are we all doomed this year? How bad is it?

I agree, it looks terrible.

But the real question is, can the U.S. go even farther into debt without things falling over?

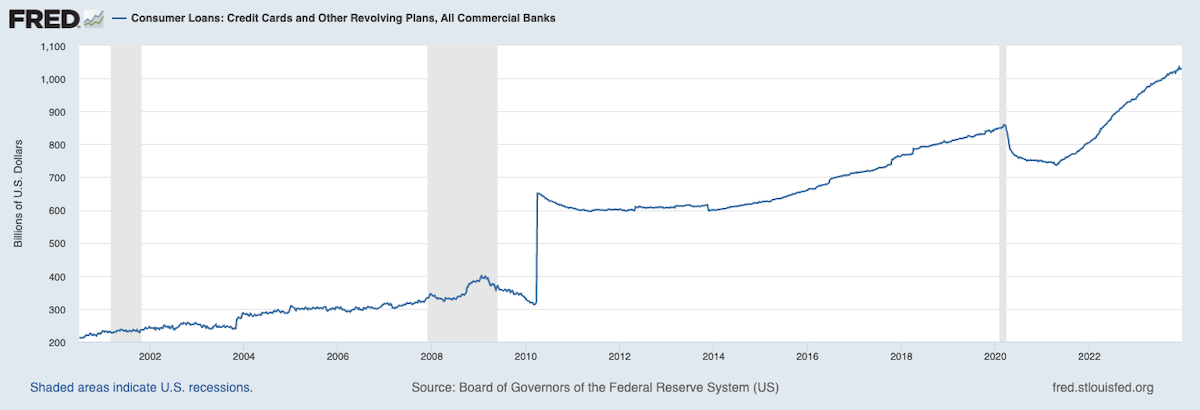

Take a look at the below chart…

In July of 2022, U.S. credit card debt reached a horrible milestone — $1 trillion.

Ominous, I know. And yet something else happened at the same time…

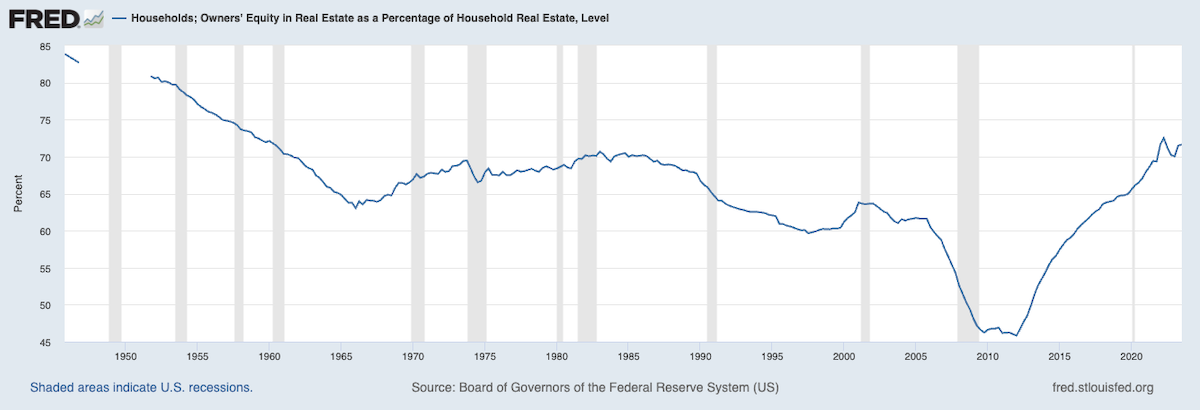

Homeowner equity in the U.S. has risen to levels that we haven’t seen since 1960.

This is the result of increased property values and the impact of inflation on property prices.

What this means is that homeowners have the ability to take out more than $10 trillion in home equity loans due to increased value of their homes.

The reality is that U.S. consumers have the ability to spend more by taking equity in their homes. Banks will be happy to lend and allow consumers to take on more debt as a result of increased real estate values.

So where does that leave us with regards to inflation?

The government and the mass media want us to believe that inflation has been whipped. They tell us everything is fine — that the problem has been solved.

The markets are also telling us that a string of rate cuts in the Fed Funds rate are in our future this year.

That suggests six or seven 25 basis points (0.25%) cuts between now and January of 2025. That would be between 150 and 175 basis points of reduction of the Fed Funds rate between now and then.

If that happened, 2024 would be an immediate “risk on,” gangbuster of a year for the stock markets. It would also guarantee the sharp recovery in small capitalization stocks.

Of course, I want this to happen. Wall Street wants this to happen.

But it won’t. It’s wishful thinking.

Despite what we hear in the news or from the government, inflation is everywhere. It hasn’t been tamed. We all feel it every day.

Whether it’s rent, gas for the car, the cost of a meal out, or our grocery bill, prices are radically higher than what they were back in 2019.

Even if we look at price increases year over year, the reality is completely different than what we’re told:

I could go on. The numbers are ridiculous. And this is after three years of constantly increasing prices.

Which means now we’re faced with a much starker reality that is the result of fiscal, monetary, and economic policy. As a result, the Federal Reserve is in a very tight spot…

Any decrease in the Fed Funds rate will result in increased spending in the market. The reason is because lower interest rates increase disposable income and increase consumer spending. That fuels more inflation.

It also results in an increase of purchases of things like real estate and automobiles, which are both interest rate sensitive.

And that’s why the Federal Reserve won’t be cutting the Fed Funds rate six or seven times in the next 12 months.

If there’s one thing we know about Fed Chair Powell, it’s that he is hell bent on shutting down inflation… no matter how much damage it has on the economy or the stock markets.

This means that if there are any interest rate cuts, they will be limited — far less than what the market has priced in. I’d say 75 basis points or less.

As long as we accept that fiscal deficits will continue to remain at ridiculous levels this year, the Federal Reserve will be forced to keep interest rates higher for a longer period of time.

The reality is that the two major contributors to inflation — supply chain problems and the labor shortage — have run their course. They’ve been accounted for. And we shouldn’t expect that they will be able to reduce inflation any further.

And the Fed — and any future rate cuts — is not only baked into current market sentiment, the market has overestimated the Fed’s ability/willingness to make such aggressive cuts.

In time, this will result in a huge disappointment once this is understood.

This is the fundamental tension that will define 2024. And it’s the one big story that the mass media has completely wrong. The Fed is in a tight spot. Inflation is here to stay this year…

And it will result in a volatile market that will be defined by both bullish and bearish runs throughout the year.

When Wall Street thinks that interest rates are going to drop significantly, it will allocate into equities. When it realizes rates aren’t coming down, it will sell. I believe we’ll see this kind of back and forth throughout the year.

Generally speaking, that means this is a trader’s market. This kind of volatility is suitable for more nimble, short-term trading, as opposed to just buying an index fund and riding out the year.

It is also going to be stock picker’s market…

Even in rough, volatile markets, there will always be sectors and individual companies that are benefiting from underlying trends, whether they are biotech breakthroughs, technological advancements, government policy driven tailwinds, or supply chain disruptions.

For example, as I wrote on December 28, 2023, this year will be the beginning of what I call manifested AI. Artificial intelligence (AI) will be manifested into forms that will be incredibly useful to the human race.

Intelligent chatbots capable of performing tasks — things that take up a considerable amount of our time throughout the day — will be widely available to consumers. Their application will be present in the workplace, as well.

These intelligent “agents” will also be manifested in hardware — forms of robotics — that will make them incredibly useful in the real world. We can think of these “robotic shells” as an interface through which AI interacts in our world.

We’re going to see the beginning of large productivity increases as a result.

In fact, the productivity jump that comes as a result of artificial intelligence will be the greatest in history. This is literally a once-in-a-generation event. And it is happening… right now.

The stakes are extremely high for humanity. If we pass through this technological gate, managing this newfound power for good, it will lead to a world of abundance and dramatically improved quality of life.

And the wealth creation that will happen for investors with exposure to this trend will also be once in a lifetime.

The reality is that no matter what happens in the markets this year, this trend is unstoppable. There are many others like it.

The companies creating or leveraging AI in a way that drives incredible productivity improvements will profit greatly, which will be reflected in their share prices.

It will also be important to allocate into private investment opportunities this year. Asset allocation into private investments — especially among the wealthy elite — continues to rise.

Over time, this is where the greatest gains are found. And companies that are pushing the outer limits of technology tend to be private and remain so for years before considering to access the public markets. They simply aren’t incentivized to go public in rough market conditions, and venture capital/private equity firms are happy to continue to fund their growth as private companies.

This has created a massive backlog of companies that will eventually go public at much higher valuations.

I believe that the IPO market will also continue to be lackluster this year, with the majority of the more interesting offerings happening the September to early December timeframe this year.

So in summary, there will be plenty of attractive investment/trading opportunities this year. It just won’t be across the board, with a market going up consistently all year.

Things that will work well this year are:

Now, with those things said, there are some major wildcards that could cause extreme chaos in the markets this year.

These are the kinds of things that we hope don’t continue, or happen in the first place, but in the current environment probably will.

One of the most underreported geopolitical events of last year was how the U.S. government committed economic warfare on Europe, primarily Germany, by intentionally taking out the Nord Stream pipelines.

For those interested, journalist Seymour Hersh did some phenomenal work this year exposing exactly what happened and how. Those interested can check out his work here.

Hersh’s work was largely ignored by the media as it was counter narrative/counter propaganda.

It’s a great example because it shows how far the deep state/administrative state will go to achieve their plans. The cost of life doesn’t matter to “them,” nor does the impact to the environment.

Consider this: The intentional detonation of the two Nord Stream pipelines released about 300,000 metric tons of methane gas into the atmosphere. It was one of the worst environmental disasters in history.

Methane gas is more than 80-times worse for the climate than carbon dioxide (plant food)…

The point is, they knew this before they blew the pipelines up. How’s that for environmental policy?

This is useful context when we think about this year. Whether we like it or not, we know how far the current administration will go to foment conflict and division.

Panic and crisis create opportunity for pushing through new spending bills for economic stimulus, enriching the military industrial complex, paying the censorship industrial complex, and creating the opportunity for money laundering and other forms of bribery and influence peddling.

To that end, major wild cards for this year are:

Again, we can only hope that none of these things happen; but we’ll have to be prepared for it if they do.

Each one of these events would impact both the economy and the markets. Several of these things happening at the same time could be disastrous.

But as depressing as these events are, ultimately they will pass.

In the short term, they can create compelling trading and investment opportunities. In the long term, hopefully we return to better geopolitical policy and a more peaceful world.

There is one final thing that we will all be well served to remember…

We are living through an extraordinary moment in time. It’s the moment when we can no longer keep track of the pace of technological development. It’s the moment when the world witnesses its first artificial general intelligence.

This simple fact means that we’re about to enter a world of abundance.

Automation enabled by AI and robotics will reduce cost of living and improve quality of life.

Endless, cheap clean energy is not far away through nuclear fusion.

Medical breakthroughs in biotech will bring a cure to most disease, and for many, the time-consuming and often stressful task of driving oneself will become a thing of the past.

What an incredible time to be alive.

If we’re smart about it, and we stay on top of these trends, we’re going to come out ahead.

Sending my best wishes for 2024,

Jeff

What do you think of this issue of Outer Limits? As always, we welcome your feedback and questions, and look forward to them. We read each and every email and address common questions in the Friday AMA issues. Please write to us by clicking here.