Earnings announcements tend not to be very interesting.

We usually expect to see a brief snapshot of the prior quarter’s financial performance, along with highlights on any strategic deals… and sometimes some forward-looking guidance.

Most of the time, the small incremental ups and downs are baked in and expected by the markets.

But every once in a while, we get a jaw-dropping earnings announcement. One that’s worthy of Outer Limits — not just because of an individual company’s performance, but because of what insights it provides us on a major trend or industry.

And that was the case for NVIDIA’s fiscal 2025 first quarter (February 1-April 28, 2024).

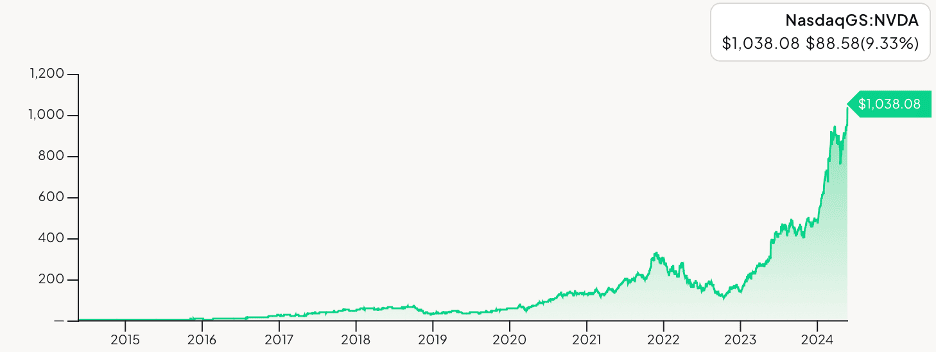

As a reminder, NVIDIA is the world’s most valuable semiconductor company, now worth an incredible $2.3 trillion.

NVIDIA is what’s known as a fabless semiconductor company, meaning that it doesn’t own or operate any semiconductor fabrication plants.

NVIDIA primarily uses Taiwan Semiconductor Manufacturing Corp (TSMC) to manufacture its semiconductors. NVIDIA therefore focuses on designing the semiconductors (the hardware) and the software used by developers that make it such a valuable company.

Today, NVIDIA is most widely known for its graphics processor units (GPUs), which became the workhorses for training artificial intelligences (AIs). The markets now recognize it as the most prominent AI company in the world. But that wasn’t always the case.

I pounded the table recommending NVIDIA back in February of 2016 at an investment conference, explaining that it wasn’t a gaming company — it was an artificial intelligence company.

My investment thesis at that time centered around NVIDIA being the most obvious company whose products would be needed to fuel the explosion in machine learning and artificial intelligence.

That trend was in its early days back then, but the signs were everywhere. And it was the constant doubling of semiconductor processing power that was the catalyst for the proliferation of AI software. Afterall, without the “horsepower,” there would be no generative AI.

And yet, the markets still considered NVIDIA a gaming company — one that produced GPUs for graphics accelerators used in PCs and game consoles so consumers could enjoy playing computer games.

It was remarkable how misunderstood NVIDIA was back then. I recommended the company at $24. On the back of yesterday’s earnings announcement, it is now trading above $1,000 a share for the first time in history.

The stock is now up more than 43X.

So what happened yesterday?

NVIDIA blew its numbers out of the water yesterday.

Those aren’t typos.

Its quarterly revenue increased 262% year over year. And its data center revenues popped 427% year over year.

It is so rare for a company of this size to be posting numbers like this.

NVIDIA literally can’t make enough semiconductors to keep up with demand. And that’s why its earnings results are so telling for what is happening right now in the world of artificial intelligence.

Its data center revenue, which is the revenue most related to artificial intelligence, is now 87% of NVIDIA’s total business.

For comparison:

When we see the breakdown, it becomes very easy to see why NVIDIA is an AI-driven company.

There had been some concern that orders might be slowing down for the current generation of high performance GPU — the GH200 Grace Hopper superchip.

The thinking was that NVIDIA’s customers would hold off on new Grace Hopper GPUs because of the forthcoming Blackwell GPUs, the next generation of superchips, which we first covered in Outer Limits — “Everything That Moves Will Become Robotic”.

The new Blackwell superchips are already in production, will start to hit the market in fiscal 2025 third quarter (starting August 2025), and be in full-scale deployment starting fiscal 2025 fourth quarter (started November 2024).

The reality of the industry and its competitive dynamics, however, are what’s driving the buying decisions. The industry can’t wait until November, or even August for that matter. It needs GPU horsepower now!

NVIDIA was very clear about the industry drivers:

“Our data center growth was fueled by strong and accelerating demand for generative AI training and inference on the Hopper platform.”

And looking forward:

“We are poised for our next wave of growth. The Blackwell platform is in full production and forms the foundation for trillion-parameter-scale generative AI.”

This may just seem like a technical specification, but what is really said is that Blackwell is the platform that will enable the training of an artificial general intelligence (AGI).

The fact is the software (the AI) can’t happen without the hardware. The hardware has to come first…

And here it is.

It’s worth asking the question, where is all this money coming from to buy GPUs?

The money behind what we’re seeing now is coming from two places:

As for the second point, given the investment flows into private artificial intelligence companies over the last several years, the bull signals could be seen from miles away.

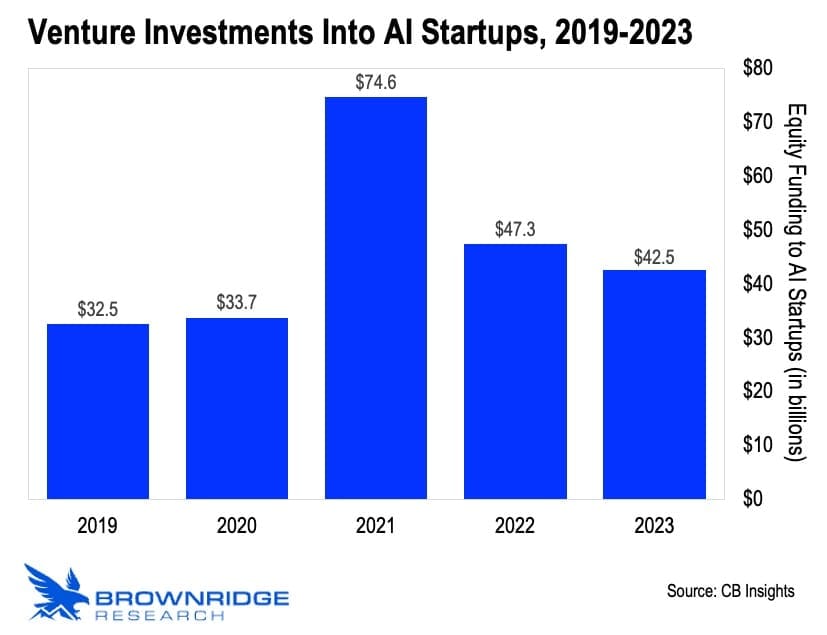

If we look back just five years, investment in AI startups kicked into high gear in 2019 at $32.5 billion, rising to a peak of $74.6 billion in 2021.

2021 was a bit of an anomaly, due to all of the pandemic-related stimulus spending. So the real “tell” was the strong numbers in 2022, a bear market, at $47.3 billion.

And while last year was down about 10% year on year, the numbers remain elevated. That’s about $230 billion invested in total over the last five years.

And most of these companies rely on NVIDIA hardware.

This is a massive secular trend that will continue for the next several years.

And the real nugget within these numbers is the explosion in investment in generative AI technology. These are the large language models (LLMs) that we’ve been exploring in Outer Limits.

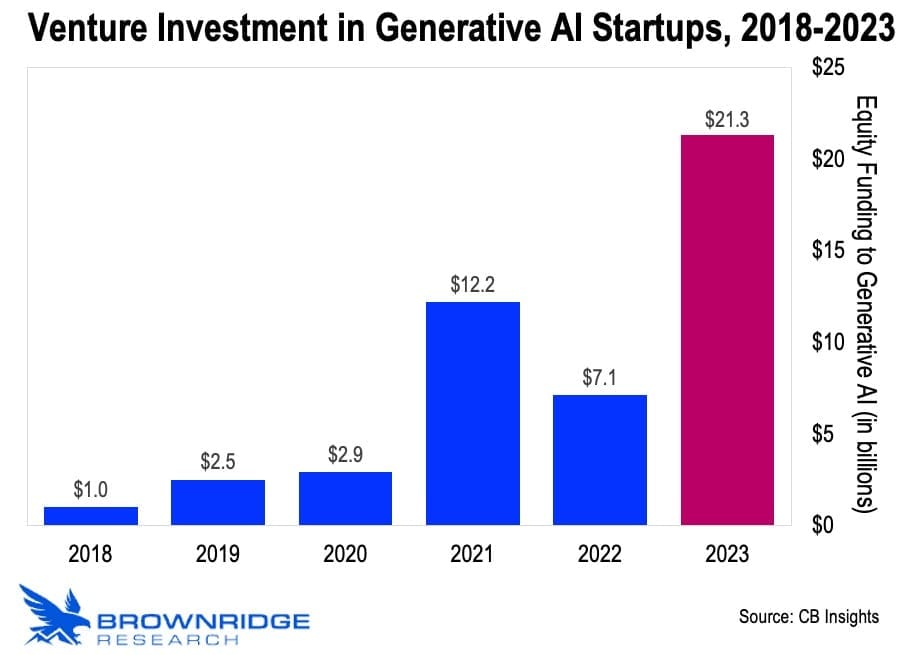

As we can see below, since 2018, generative AI sprung from just $1 billion in investment to $12.2 billion in 2021, to $21.3 billion in 2023.

Admittedly, last year was a massive year for generative AI investments. But it was largely driven by investments made by Microsoft and Amazon.

The deal of the year was the additional $10 billion that Microsoft allocated into OpenAI, followed by $1.3 billion into Inflection AI, and Amazon’s $4 billion into Anthropic.

But who says there won’t be more? This is a race to artificial general intelligence — a multi-trillion dollar opportunity.

It’s not just the large tech companies with loads of cash swinging for the fences. Nation states are scrambling to employ this technology.

And whether or not it is a company or a government, not adopting artificial intelligence is quickly becoming a severe disadvantage.

As for NVIDIA, it gave forward guidance of $28 billion +/- 2% for the current fiscal quarter. No matter where it ends up, it will be another record quarter.

And the icing on the cake was the announcement that NVIDIA will implement a 10:1 stock split on June 7. Every ten shares will be worth 1 of the new shares, resulting in a share price that will trade around $100 at current levels.

As a reminder, the valuation of the company does not change with a stock split like this. Shares just appear to be cheaper to some because of the lower nominal share price. These splits tend to bring in additional retail capital for that reason.

Investing at these levels is a pure momentum play right now. Valuations for NVIDIA are sky high, but if the semiconductor giant keeps shattering records quarter after quarter, it’s possible to ride higher from here.

We always welcome your feedback. We read every email and address the most common comments and questions in the Friday AMA. Please write to us here.